The value of Bitcoin has had its ups and downs since its inception in 2013, but its recent skyrocket in value has created renewed interest in this virtual currency. The rapid growth of this alternative currency has dominated headlines and ignited a cryptocurrency boom that has consumers everywhere wondering how to get a slice of the Bitcoin pie. For those who want to join the craze without trading traditional currencies like U.S. dollars (i.e., fiat currency), a process called Bitcoin mining is an entry point. However, Bitcoin mining poses a number of security risks that you need to know.

Mining for Bitcoin is like mining for gold—you put in the work and you get your reward. But instead of back-breaking labor, you earn the currency with your time and computer processing power. Miners, as they are called, essentially maintain and secure Bitcoin’s decentralized accounting system. Bitcoin transactions are recorded in a digital ledger called a blockchain. Bitcoin miners update the ledger by downloading a special piece of software that allows them to verify and collect new transactions. Then, they must solve a mathematical puzzle to secure access to add a block of transactions to the chain. In return, they earn Bitcoins, as well as a transaction fee.

As the digital currency has matured, Bitcoin mining has become more challenging. In the beginning, a Bitcoin user could mine on their home computer and earn a good amount of the digital currency, but these days the math problems have become so complicated that it requires a lot of expensive computing power. This is where the risks come in. Since miners need an increasing amount of computer power to earn Bitcoin, some have started compromising public Wi-Fi networks so they can access users’ devices.

One example of this security breach happened at a coffee shop in Buenos Aires, which was infected with malware that caused a 10-second delay when logging in to the cafe’s Wi-Fi network. The malware authors used this time delay to access the users’ laptops for mining. In addition to public Wi-Fi networks, millions of websites are being compromised to access users’ devices for mining. When an attacker loads mining software onto devices without the owner’s permission, it’s called a cryptocurrency mining encounter or cryptojacking.

It’s estimated that 50 out of every 100,000 devices have encountered a cryptocurrency miner. Cryptojacking is a widespread problem and can slow down your device; though, that’s not the worst that can happen. Utility costs are also likely to go through the roof. A device that is cryptojacked could have 100 percent of its resources used for mining, causing the device to overheat, essentially destroying it.

Now that you know a little about mining and the Bitcoin security risks associated with it, here are some tips to keep your devices safe as you monitor the cryptocurrency market:

The post Bitcoin Security: Mining Threats You Need to Know appeared first on McAfee Blog.

The recent mass-theft of authentication tokens from Salesloft, whose AI chatbot is used by a broad swath of corporate America to convert customer interaction into Salesforce leads, has left many companies racing to invalidate the stolen credentials before hackers can exploit them. Now Google warns the breach goes far beyond access to Salesforce data, noting the hackers responsible also stole valid authentication tokens for hundreds of online services that customers can integrate with Salesloft, including Slack, Google Workspace, Amazon S3, Microsoft Azure, and OpenAI.

Salesloft says its products are trusted by 5,000+ customers. Some of the bigger names are visible on the company’s homepage.

Salesloft disclosed on August 20 that, “Today, we detected a security issue in the Drift application,” referring to the technology that powers an AI chatbot used by so many corporate websites. The alert urged customers to re-authenticate the connection between the Drift and Salesforce apps to invalidate their existing authentication tokens, but it said nothing then to indicate those tokens had already been stolen.

On August 26, the Google Threat Intelligence Group (GTIG) warned that unidentified hackers tracked as UNC6395 used the access tokens stolen from Salesloft to siphon large amounts of data from numerous corporate Salesforce instances. Google said the data theft began as early as Aug. 8, 2025 and lasted through at least Aug. 18, 2025, and that the incident did not involve any vulnerability in the Salesforce platform.

Google said the attackers have been sifting through the massive data haul for credential materials such as AWS keys, VPN credentials, and credentials to the cloud storage provider Snowflake.

“If successful, the right credentials could allow them to further compromise victim and client environments, as well as pivot to the victim’s clients or partner environments,” the GTIG report stated.

The GTIG updated its advisory on August 28 to acknowledge the attackers used the stolen tokens to access email from “a very small number of Google Workspace accounts” that were specially configured to integrate with Salesloft. More importantly, it warned organizations to immediately invalidate all tokens stored in or connected to their Salesloft integrations — regardless of the third-party service in question.

“Given GTIG’s observations of data exfiltration associated with the campaign, organizations using Salesloft Drift to integrate with third-party platforms (including but not limited to Salesforce) should consider their data compromised and are urged to take immediate remediation steps,” Google advised.

On August 28, Salesforce blocked Drift from integrating with its platform, and with its productivity platforms Slack and Pardot.

The Salesloft incident comes on the heels of a broad social engineering campaign that used voice phishing to trick targets into connecting a malicious app to their organization’s Salesforce portal. That campaign led to data breaches and extortion attacks affecting a number of companies including Adidas, Allianz Life and Qantas.

On August 5, Google disclosed that one of its corporate Salesforce instances was compromised by the attackers, which the GTIG has dubbed UNC6040 (“UNC” stands for “uncategorized threat group”). Google said the extortionists consistently claimed to be the threat group ShinyHunters, and that the group appeared to be preparing to escalate its extortion attacks by launching a data leak site.

ShinyHunters is an amorphous threat group known for using social engineering to break into cloud platforms and third-party IT providers, and for posting dozens of stolen databases to cybercrime communities like the now-defunct Breachforums.

The ShinyHunters brand dates back to 2020, and the group has been credited with or taken responsibility for dozens of data leaks that exposed hundreds of millions of breached records. The group’s member roster is thought to be somewhat fluid, drawing mainly from active denizens of the Com, a mostly English-language cybercrime community scattered across an ocean of Telegram and Discord servers.

Recorded Future’s Alan Liska told Bleeping Computer that the overlap in the “tools, techniques and procedures” used by ShinyHunters and the Scattered Spider extortion group likely indicate some crossover between the two groups.

To muddy the waters even further, on August 28 a Telegram channel that now has nearly 40,000 subscribers was launched under the intentionally confusing banner “Scattered LAPSUS$ Hunters 4.0,” wherein participants have repeatedly claimed responsibility for the Salesloft hack without actually sharing any details to prove their claims.

The Telegram group has been trying to attract media attention by threatening security researchers at Google and other firms. It also is using the channel’s sudden popularity to promote a new cybercrime forum called “Breachstars,” which they claim will soon host data stolen from victim companies who refuse to negotiate a ransom payment.

The “Scattered Lapsus$ Hunters 4.0” channel on Telegram now has roughly 40,000 subscribers.

But Austin Larsen, a principal threat analyst at Google’s threat intelligence group, said there is no compelling evidence to attribute the Salesloft activity to ShinyHunters or to other known groups at this time.

“Their understanding of the incident seems to come from public reporting alone,” Larsen told KrebsOnSecurity, referring to the most active participants in the Scattered LAPSUS$ Hunters 4.0 Telegram channel.

Joshua Wright, a senior technical director at Counter Hack, is credited with coining the term “authorization sprawl” to describe one key reason that social engineering attacks from groups like Scattered Spider and ShinyHunters so often succeed: They abuse legitimate user access tokens to move seamlessly between on-premises and cloud systems.

Wright said this type of attack chain often goes undetected because the attacker sticks to the resources and access already allocated to the user.

“Instead of the conventional chain of initial access, privilege escalation and endpoint bypass, these threat actors are using centralized identity platforms that offer single sign-on (SSO) and integrated authentication and authorization schemes,” Wright wrote in a June 2025 column. “Rather than creating custom malware, attackers use the resources already available to them as authorized users.”

It remains unclear exactly how the attackers gained access to all Salesloft Drift authentication tokens. Salesloft announced on August 27 that it hired Mandiant, Google Cloud’s incident response division, to investigate the root cause(s).

“We are working with Salesloft Drift to investigate the root cause of what occurred and then it’ll be up to them to publish that,” Mandiant Consulting CTO Charles Carmakal told Cyberscoop. “There will be a lot more tomorrow, and the next day, and the next day.”

Carding — the underground business of stealing, selling and swiping stolen payment card data — has long been the dominion of Russia-based hackers. Happily, the broad deployment of more secure chip-based payment cards in the United States has weakened the carding market. But a flurry of innovation from cybercrime groups in China is breathing new life into the carding industry, by turning phished card data into mobile wallets that can be used online and at main street stores.

An image from one Chinese phishing group’s Telegram channel shows various toll road phish kits available.

If you own a mobile phone, the chances are excellent that at some point in the past two years it has received at least one phishing message that spoofs the U.S. Postal Service to supposedly collect some outstanding delivery fee, or an SMS that pretends to be a local toll road operator warning of a delinquent toll fee.

These messages are being sent through sophisticated phishing kits sold by several cybercriminals based in mainland China. And they are not traditional SMS phishing or “smishing” messages, as they bypass the mobile networks entirely. Rather, the missives are sent through the Apple iMessage service and through RCS, the functionally equivalent technology on Google phones.

People who enter their payment card data at one of these sites will be told their financial institution needs to verify the small transaction by sending a one-time passcode to the customer’s mobile device. In reality, that code will be sent by the victim’s financial institution to verify that the user indeed wishes to link their card information to a mobile wallet.

If the victim then provides that one-time code, the phishers will link the card data to a new mobile wallet from Apple or Google, loading the wallet onto a mobile phone that the scammers control.

Ford Merrill works in security research at SecAlliance, a CSIS Security Group company. Merrill has been studying the evolution of several China-based smishing gangs, and found that most of them feature helpful and informative video tutorials in their sales accounts on Telegram. Those videos show the thieves are loading multiple stolen digital wallets on a single mobile device, and then selling those phones in bulk for hundreds of dollars apiece.

“Who says carding is dead?,” said Merrill, who presented about his findings at the M3AAWG security conference in Lisbon earlier today. “This is the best mag stripe cloning device ever. This threat actor is saying you need to buy at least 10 phones, and they’ll air ship them to you.”

One promotional video shows stacks of milk crates stuffed full of phones for sale. A closer inspection reveals that each phone is affixed with a handwritten notation that typically references the date its mobile wallets were added, the number of wallets on the device, and the initials of the seller.

An image from the Telegram channel for a popular Chinese smishing kit vendor shows 10 mobile phones for sale, each loaded with 4-6 digital wallets from different UK financial institutions.

Merrill said one common way criminal groups in China are cashing out with these stolen mobile wallets involves setting up fake e-commerce businesses on Stripe or Zelle and running transactions through those entities — often for amounts totaling between $100 and $500.

Merrill said that when these phishing groups first began operating in earnest two years ago, they would wait between 60 to 90 days before selling the phones or using them for fraud. But these days that waiting period is more like just seven to ten days, he said.

“When they first installed this, the actors were very patient,” he said. “Nowadays, they only wait like 10 days before [the wallets] are hit hard and fast.”

Criminals also can cash out mobile wallets by obtaining real point-of-sale terminals and using tap-to-pay on phone after phone. But they also offer a more cutting-edge mobile fraud technology: Merrill found that at least one of the Chinese phishing groups sells an Android app called “ZNFC” that can relay a valid NFC transaction to anywhere in the world. The user simply waves their phone at a local payment terminal that accepts Apple or Google pay, and the app relays an NFC transaction over the Internet from a phone in China.

“The software can work from anywhere in the world,” Merrill said. “These guys provide the software for $500 a month, and it can relay both NFC enabled tap-to-pay as well as any digital wallet. They even have 24-hour support.”

The rise of so-called “ghost tap” mobile software was first documented in November 2024 by security experts at ThreatFabric. Andy Chandler, the company’s chief commercial officer, said their researchers have since identified a number of criminal groups from different regions of the world latching on to this scheme.

Chandler said those include organized crime gangs in Europe that are using similar mobile wallet and NFC attacks to take money out of ATMs made to work with smartphones.

“No one is talking about it, but we’re now seeing ten different methodologies using the same modus operandi, and none of them are doing it the same,” Chandler said. “This is much bigger than the banks are prepared to say.”

A November 2024 story in the Singapore daily The Straits Times reported authorities there arrested three foreign men who were recruited in their home countries via social messaging platforms, and given ghost tap apps with which to purchase expensive items from retailers, including mobile phones, jewelry, and gold bars.

“Since Nov 4, at least 10 victims who had fallen for e-commerce scams have reported unauthorised transactions totaling more than $100,000 on their credit cards for purchases such as electronic products, like iPhones and chargers, and jewelry in Singapore,” The Straits Times wrote, noting that in another case with a similar modus operandi, the police arrested a Malaysian man and woman on Nov 8.

Three individuals charged with using ghost tap software at an electronics store in Singapore. Image: The Straits Times.

According to Merrill, the phishing pages that spoof the USPS and various toll road operators are powered by several innovations designed to maximize the extraction of victim data.

For example, a would-be smishing victim might enter their personal and financial information, but then decide the whole thing is scam before actually submitting the data. In this case, anything typed into the data fields of the phishing page will be captured in real time, regardless of whether the visitor actually clicks the “submit” button.

Merrill said people who submit payment card data to these phishing sites often are then told their card can’t be processed, and urged to use a different card. This technique, he said, sometimes allows the phishers to steal more than one mobile wallet per victim.

Many phishing websites expose victim data by storing the stolen information directly on the phishing domain. But Merrill said these Chinese phishing kits will forward all victim data to a back-end database operated by the phishing kit vendors. That way, even when the smishing sites get taken down for fraud, the stolen data is still safe and secure.

Another important innovation is the use of mass-created Apple and Google user accounts through which these phishers send their spam messages. One of the Chinese phishing groups posted images on their Telegram sales channels showing how these robot Apple and Google accounts are loaded onto Apple and Google phones, and arranged snugly next to each other in an expansive, multi-tiered rack that sits directly in front of the phishing service operator.

The ashtray says: You’ve been phishing all night.

In other words, the smishing websites are powered by real human operators as long as new messages are being sent. Merrill said the criminals appear to send only a few dozen messages at a time, likely because completing the scam takes manual work by the human operators in China. After all, most one-time codes used for mobile wallet provisioning are generally only good for a few minutes before they expire.

Notably, none of the phishing sites spoofing the toll operators or postal services will load in a regular Web browser; they will only render if they detect that a visitor is coming from a mobile device.

“One of the reasons they want you to be on a mobile device is they want you to be on the same device that is going to receive the one-time code,” Merrill said. “They also want to minimize the chances you will leave. And if they want to get that mobile tokenization and grab your one-time code, they need a live operator.”

Merrill found the Chinese phishing kits feature another innovation that makes it simple for customers to turn stolen card details into a mobile wallet: They programmatically take the card data supplied by the phishing victim and convert it into a digital image of a real payment card that matches that victim’s financial institution. That way, attempting to enroll a stolen card into Apple Pay, for example, becomes as easy as scanning the fabricated card image with an iPhone.

An ad from a Chinese SMS phishing group’s Telegram channel showing how the service converts stolen card data into an image of the stolen card.

“The phone isn’t smart enough to know whether it’s a real card or just an image,” Merrill said. “So it scans the card into Apple Pay, which says okay we need to verify that you’re the owner of the card by sending a one-time code.”

How profitable are these mobile phishing kits? The best guess so far comes from data gathered by other security researchers who’ve been tracking these advanced Chinese phishing vendors.

In August 2023, the security firm Resecurity discovered a vulnerability in one popular Chinese phish kit vendor’s platform that exposed the personal and financial data of phishing victims. Resecurity dubbed the group the Smishing Triad, and found the gang had harvested 108,044 payment cards across 31 phishing domains (3,485 cards per domain).

In August 2024, security researcher Grant Smith gave a presentation at the DEFCON security conference about tracking down the Smishing Triad after scammers spoofing the U.S. Postal Service duped his wife. By identifying a different vulnerability in the gang’s phishing kit, Smith said he was able to see that people entered 438,669 unique credit cards in 1,133 phishing domains (387 cards per domain).

Based on his research, Merrill said it’s reasonable to expect between $100 and $500 in losses on each card that is turned into a mobile wallet. Merrill said they observed nearly 33,000 unique domains tied to these Chinese smishing groups during the year between the publication of Resecurity’s research and Smith’s DEFCON talk.

Using a median number of 1,935 cards per domain and a conservative loss of $250 per card, that comes out to about $15 billion in fraudulent charges over a year.

Merrill was reluctant to say whether he’d identified additional security vulnerabilities in any of the phishing kits sold by the Chinese groups, noting that the phishers quickly fixed the vulnerabilities that were detailed publicly by Resecurity and Smith.

Adoption of touchless payments took off in the United States after the Coronavirus pandemic emerged, and many financial institutions in the United States were eager to make it simple for customers to link payment cards to mobile wallets. Thus, the authentication requirement for doing so defaulted to sending the customer a one-time code via SMS.

Experts say the continued reliance on one-time codes for onboarding mobile wallets has fostered this new wave of carding. KrebsOnSecurity interviewed a security executive from a large European financial institution who spoke on condition of anonymity because they were not authorized to speak to the press.

That expert said the lag between the phishing of victim card data and its eventual use for fraud has left many financial institutions struggling to correlate the causes of their losses.

“That’s part of why the industry as a whole has been caught by surprise,” the expert said. “A lot of people are asking, how this is possible now that we’ve tokenized a plaintext process. We’ve never seen the volume of sending and people responding that we’re seeing with these phishers.”

To improve the security of digital wallet provisioning, some banks in Europe and Asia require customers to log in to the bank’s mobile app before they can link a digital wallet to their device.

Addressing the ghost tap threat may require updates to contactless payment terminals, to better identify NFC transactions that are being relayed from another device. But experts say it’s unrealistic to expect retailers will be eager to replace existing payment terminals before their expected lifespans expire.

And of course Apple and Google have an increased role to play as well, given that their accounts are being created en masse and used to blast out these smishing messages. Both companies could easily tell which of their devices suddenly have 7-10 different mobile wallets added from 7-10 different people around the world. They could also recommend that financial institutions use more secure authentication methods for mobile wallet provisioning.

Neither Apple nor Google responded to requests for comment on this story.

A ransomware group called Dark Angels made headlines this past week when it was revealed the crime group recently received a record $75 million data ransom payment from a Fortune 50 company. Security experts say the Dark Angels have been around since 2021, but the group doesn’t get much press because they work alone and maintain a low profile, picking one target at a time and favoring mass data theft over disrupting the victim’s operations.

Image: Shutterstock.

Security firm Zscaler ThreatLabz this month ranked Dark Angels as the top ransomware threat for 2024, noting that in early 2024 a victim paid the ransomware group $75 million — higher than any previously recorded ransom payment. ThreatLabz found Dark Angels has conducted some of the largest ransomware attacks to date, and yet little is known about the group.

Brett Stone-Gross, senior director of threat intelligence at ThreatLabz, said Dark Angels operate using an entirely different playbook than most other ransomware groups. For starters, he said, Dark Angels does not employ the typical ransomware affiliate model, which relies on hackers-for-hire to install malicious software that locks up infected systems.

“They really don’t want to be in the headlines or cause business disruptions,” Stone-Gross said. “They’re about making money and attracting as little attention as possible.”

Most ransomware groups maintain flashy victim leak sites which threaten to publish the target’s stolen data unless a ransom demand is paid. But the Dark Angels didn’t even have a victim shaming site until April 2023. And the leak site isn’t particularly well branded; it’s called Dunghill Leak.

The Dark Angels victim shaming site, Dunghill Leak.

“Nothing about them is flashy,” Stone-Gross said. “For the longest time, they didn’t even want to cause a big headline, but they probably felt compelled to create that leaks site because they wanted to show they were serious and that they were going to post victim data and make it accessible.”

Dark Angels is thought to be a Russia-based cybercrime syndicate whose distinguishing characteristic is stealing truly staggering amounts of data from major companies across multiple sectors, including healthcare, finance, government and education. For large businesses, the group has exfiltrated between 10-100 terabytes of data, which can take days or weeks to transfer, ThreatLabz found.

Like most ransom gangs, Dark Angels will publish data stolen from victims who do not pay. Some of the more notable victims listed on Dunghill Leak include the global food distribution firm Sysco, which disclosed a ransomware attack in May 2023; and the travel booking giant Sabre, which was hit by the Dark Angels in September 2023.

Stone-Gross said Dark Angels is often reluctant to deploy ransomware malware because such attacks work by locking up the target’s IT infrastructure, which typically causes the victim’s business to grind to a halt for days, weeks or even months on end. And those types of breaches tend to make headlines quickly.

“They selectively choose whether they want to deploy ransomware or not,” he said. “If they deem they can encrypt some files that won’t cause major disruptions — but will give them a ton of data — that’s what they’ll do. But really, what separates them from the rest is the volume of data they’re stealing. It’s a whole order of magnitude greater with Dark Angels. Companies losing vast amounts of data will pay these high ransoms.”

So who paid the record $75 million ransom? Bleeping Computer posited on July 30 that the victim was the pharmaceutical giant Cencora (formerly AmeriSourceBergen Corporation), which reported a data security incident to the U.S. Securities and Exchange Commission (SEC) on February 21, 2024.

The SEC requires publicly-traded companies to disclose a potentially material cybersecurity event within four days of the incident. Cencora is currently #10 on the Fortune 500 list, generating more than $262 billion in revenue last year.

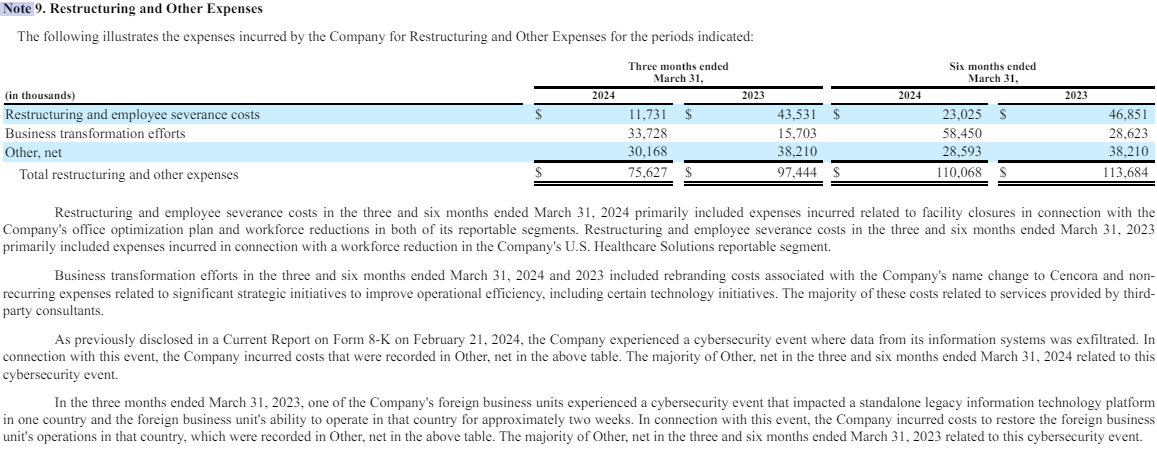

Cencora did not respond to questions about whether it had made a ransom payment in connection with the February cybersecurity incident, and referred KrebsOnSecurity to expenses listed under “Other” in the restructuring section of their latest quarterly financial report (PDF). That report states that the majority of the $30 million cost in “Other” was associated with the breach.

Cencora’s quarterly statement said the incident affected a standalone legacy information technology platform in one country and the foreign business unit’s ability to operate in that country for approximately two weeks.

Cencora’s 2024 1st quarter report documents a $30 million cost associated with a data exfiltration event in mid-February 2024.

In its most recent State of Ransomware report (PDF), security firm Sophos found the average ransomware payment had increased fivefold in the past year, from $400,000 in 2023 to $2 million. Sophos says that in more than four-fifths (82%) of cases funding for the ransom came from multiple sources. Overall, 40% of total ransom funding came from the organizations themselves and 23% from insurance providers.

Further reading: ThreatLabz ransomware report (PDF).